Last week, in a (virtual) entrepreneurial finance class at Harvard Business School, our professor pointed to a graph of IPO’s over the last several decades with various kinks in the graph and asked for explanations of what caused peaks and troughs at different points in time: “can anyone explain why there is a big upshoot in the 1960’s? What all contributed to a downward trend in the early 2000’s?”

As I raised my virtual Zoom hand to participate, I couldn’t help but reflect on the idea that 50 years from now, when students at Harvard Business School look back at time series data around the economy and the labor market, COVID-19 may have induced the single most impactful economic shift in modern history.

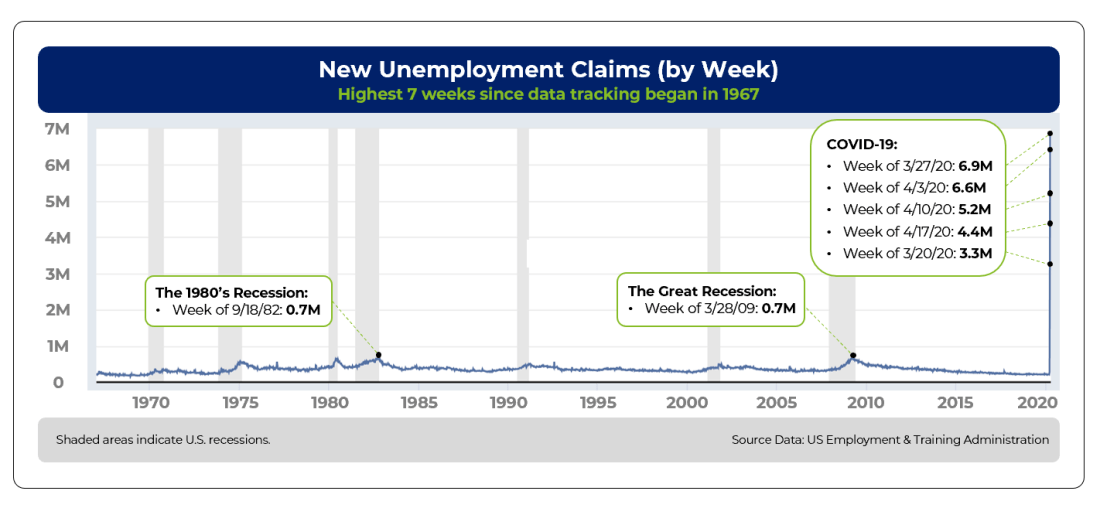

Even as I type that sentence, I am wary that it comes off with a tone that feels like it must be somewhat hyperbolic. But then you pause and stare at the below graph for 30 seconds.

At the peak of the 2008-2009 recession, there were 665,000 new unemployment claims in a week. Over the last 5 weeks, there were 3.3 Million, 6.9 Million, 6.6 Million, 5.2 Million, and 4.4 Million new unemployment claims. In the matter of only a few weeks, over 26 Million Americans lost their jobs, and the cumulative job gains over the last decade were wiped out. To say this is unprecedented is a gross understatement.

Even still, there is a lot of hysteria right now with the commotion of many speculating how exactly the future of work will be transformed. We need to separate the signal from the noise.

The Noise

A quick scan of Twitter quickly produces a plethora of worried sentiments about the labor market — internships are being revoked, full-time hiring is being frozen, the stock market is barrelling up and down, companies are moving to remote work.

Though these dynamics are certainly notable, and in some cases will cause significant pain, it’s important to realize that many of these challenges will pass and won’t be the longer-term implications of COVID-19 on the future of work.

Sure, remote work will continue to be increasingly popular, especially with droves of new enterprise software apps that make the experience more productive. But post-COVID-19 (including the potentially extended recovery), the same pros and cons of remote work will continue to exist, and though we will have seen a solid bump in employer acceptance, we will largely return to a similar balance.

The stock market is an important measure of the overall economy for a plethora of reasons, but we also need to understand that it is in many ways separate from the economic mobility of an American worker — the stock market represents (our own perception of) the value of corporations, which can lead to wide disparities between, in the words of Jim Kramer (pictured below), “a roaring stock market and an obliterated job market”.

Some might rationally ask, ‘well what does the data say” — and that’s part of the problem. We don’t have the data tracking infrastructure in place to understand our current economy and how it will be impacted by the pandemic.

The unemployment rate and other BLS measures will not capture the full scope of economic harm that is done by COVID-19. Tens of millions of Americans have had their hours and income significantly reduced, have been ‘furloughed’ (temporarily laid off) or changed to part time, have been forced to take on lower-wage jobs in the gig economy with no stability, or have have been permanently laid off, and though they want to work, believe no job is available for them (‘discouraged workers’). Zero of these people will be counted in the unemployment rate, and the BLS continues not to track income or hours and not provide adequate measures of the true size of the gig economy.

So all in all, we are left struggling to understand what to pay attention to amidst all the economic noise (and lack of the right noise) in interpreting the health and structure of our workforce.

The Signals

If we sift through all of the intensity of the short-term noise, it starts to become clear that there are a few broader future of work trends occuring that are going to be massively accelerated with the economic collapse in the wake of COVID-19.

To be clear, none of these trends are new — but the important insight is that this recession will rapidly and dramatically accelerate these trends to levels that will have a significant and permanent impact on the structure of the labor market.

- Employers will accelerate automation to fill the roles of laid off workers

In recent days, many inside and outside of our government have focused on how we can achieve the objective of ‘Getting Americans Back to Work’. The problem is, most of the plans released around this objective seem to have the implicit assumption that re-opening the economy will put the vast majority of Americans who have been laid off back to work. The reality is, many employers, even when they reach pre-crisis revenue numbers, will not employ pre-crisis levels of workers.

As a number of economists have proven, there is a strong correlation between economic recessions and a rise in employer adoption of increased automation. Their research suggests that during recessions, employers tend to lay off less skilled employees and replace them with a combination of technology and a fewer number of higher skilled workers.

This time will be no exception. In fact, it will likely be much worse. Since the 2008 recession, not only has the power of artificial intelligence, robotics, and other technologies risen at an exponential rate, they have also continued to become dramatically cheaper. This time, the tradeoff for employers will be a much easier decision.

- Individuals will need to gain new skills through innovative retraining programs to re-enter the workforce

As employers increasingly look to automation to fill the roles of laid off workers, many individuals will need to re-evaluate their skill sets before re-entering the workforce.

In general, the counter-cyclicality of education is well documented — But given the rapid acceleration of automation mentioned above, the ‘skills gap’ – the gap between the skills the individuals have and the skills employers will demand – will be much higher than in previous recessions, significantly increasing friction in the labor market. That said, individuals will be hesitant to flock to traditional higher education institutions, with skepticism over their ROI at an all time high.

Instead, new retraining models must be built that are dramatically more connected to the workforce and shift financial risk off students (a concept I’ve written about before) through ISA’s, deferred tuition, employer-sponsored, apprenticeships and other innovative models — long gone are the days where students cough up thousands of dollars upfront for programs that may or may not generate a positive employment outcome.

Additionally, retraining programs must ensure student success by providing the flexibility and support that will maximize program completion — in the age of learning when many adult learners will need to pick up part time work to continue to support their families while they retrain, it’s crucial that the programs be flexible in the “when” and the “where” of learning, in stark contrast to many of the rigid programs in higher education today. NextStep, a CNA retraining program in Colorado, is a prime example of a program offering this flexibility, with asynchronous, bite-sized lessons on a mobile-first platform.

- A sub-standard social safety net will force people into the gig economy, where they will lose the stability and benefits of full time employment

With people displaced from the workforce and unable to re-enter it without new skills, combined with basic living costs of housing, health care, education continuing to soar, inequality is likely to rise and the inadequacies of America’s social safety net are likely to be exposed. With this, we will see increasing calls for some form of universal basic income

As people who have been displaced from the labor market (and even those who haven’t) struggle to cover their expenses, they will increasingly look to the gig economy to gain quick access to income. Many (not all) gig economy platforms have low barriers to entry for workers given most of the tasks involve low-skill activities like driving, shopping, and delivering.

Even in the first few weeks of the pandemic, the flooding towards the gig economy has already begun — from individuals searching for primary as well as secondary sources of income. While it took Instacart 8 years to bring its first 200,000 shoppers on the platform, over 300,000 new shoppers joined the platform just in the past month. Though the gig economy can be attractive in the flexibility it offers, it also has meaningful disadvantages in comparison to full time employment (from income stability, to benefits, to upward mobility) that will cause substantial pain to workers in the long-term.

New social safety net models must be built, particularly those targeting gig economy workers, to provide them short-term stability and empower them to pursue long-term economic mobility. Encouraging models like Catch, Steady, and Wonolo are beginning to emerge, but are still not sufficient — the gig economy needs an entire infrastructure around it that recognizes and supports a unique class of workers.

COVID-19 is accelerating these Future of Work trends that won’t just be a short-term kink in a graph, but rather, a transformational shift in the trajectory of the economy. While the first two signals identified have been observed, to some degree, in past recessions, the rapid degree of technological progress and massive widening of the skills gap compared to past recessions will be the differences that make the trends in this recession much more impactful and enduring.

As we weather that storm, it is essential that we are able to understand the evolving health and structure of the economy. When companies and their business models evolve, so do their key metrics, but as our economy continues to transform dramatically, the Bureau of Labor Statistics continues to focus on many of the same metrics that it did a century ago. We need innovative new ways to understand the lives of workers on the ground to successfully navigate this fast-moving labor market. 60Decibels is one company that is doing interesting work with potential relation to this need, amplifying voices as part of an impact measurement tool, but there is a need for more innovations, from both the private and public sector, that specifically allow us to understand the future of work.

With every crisis, there is opportunity. The COVID-19 crisis creates significant opportunity for new models of economic mobility that support displaced workers. In light of Marc Andreessen’s recent manifesto on why it’s time to build — to empower individuals in the future of work, we need to build the data infrastructure to understand our labor market, we need to build innovative retraining programs that shift financial risk off students, and we need to build new safety nets and support systems, particularly for a growing number of independent workers.

Let’s start building.

Insightful post – your third point, regarding a loss of stability and benefits of full-time employment, is a really interesting one, especially when viewed through the lens of health insurance (often the largest “benefit” financially and most important to employees). I believe your point about new safety net models is a good one, but also anticipate that this economic environment will catalyze a shift to more employer-agnostic coverage (just like is commonplace in auto and home insurance markets). An additional driver here will be health care providers demanding alternative payment models to mitigate some of the volume risk experienced in the past couple of months.

LikeLike

Very good and very concise!!

John Bracaglia | 610-937-2023 | Harvard Business School * *

*My Website & Blog:* john-bracaglia.com *My Music: * soundcloud.com/bison-dj

On Thu, Apr 23, 2020 at 3:18 PM The Robots are Coming wrote:

> Taylor Stockton posted: ” Last week, in a (virtual) entrepreneurial > finance class at Harvard Business School, our professor pointed to a graph > of IPO’s over the last several decades with various kinks in the graph and > asked for explanations of what caused peaks and troughs at di” >

LikeLike